Audit Information

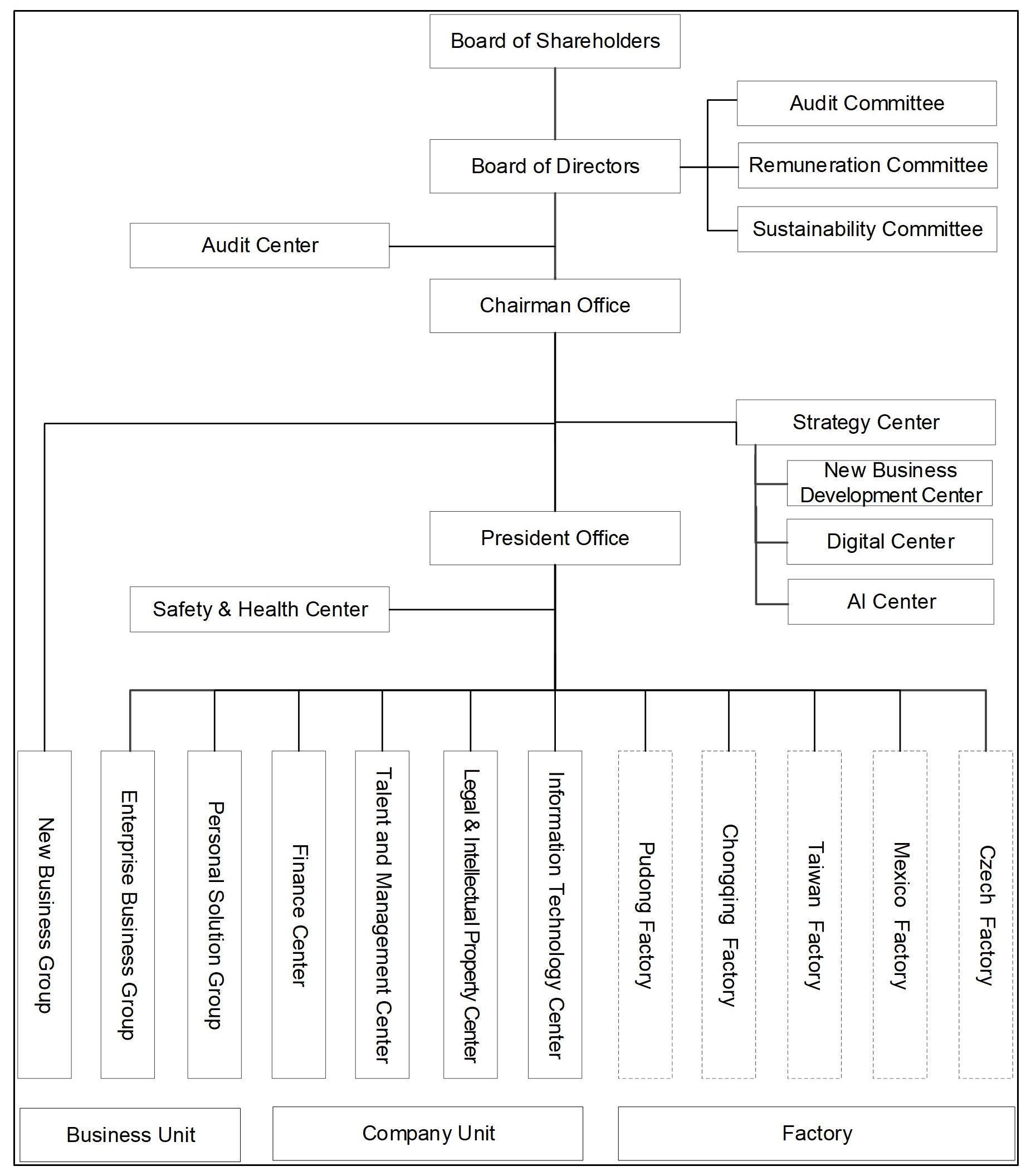

Organization chart

Scope of work of the Audit Center

The audit center is directly under board of directors and job description as follows:- To assess the internal control system of the Corporation and its subsidiaries.

- To assess whether the plans and operating procedures are efficient enough to achieve the goals of the Corporation.

- To ensure the reliability and integrity of financial and operating information, and to audit whether the controls over record keeping and reporting are adequate, effective, and timely.

- To audit whether the managers have set up standards to evaluate the economy and efficiency of manpower, equipments,materials and other resources , and have found the ways to improve it as well.

- To evaluate whether the operating standards and procedures set by management are complying with applicable laws and regulations, and to ensure that management has taken actions to prevent or correct any bias behavior.

- To review whether the management has established appropriate means to safeguard assets from various types of losses such as those resulting from theft, fire, improper or illegal activities, and exposure to the elements.

- To review the reliability of regular inventory taking procedures, and to verify the existence of assets by random checking.

- To disclose the violations of operating team to violate "Internal audit reward and punishment measures."

- To take the education and training of staff to implement prevention (risk control) internal control and self-examination.

- To review the self-inspection reports prepared by all departments and subsidiaries and all other affairs handed by the authorities.

Design and Operation of Internal Control Systems

(1).Valuation of board of directors:

Do the right thing in the first time, as to avoid repeated negligence, waste and errors caused for the loss of company resources. Board of directors of Inventec passed a "Internal audit reward and punishment measures" in August 2006. If the employee violates the rules may be punished ,which will affect individual bonuses and promotion opportunities.

(2).Operations of Internal Audit:

According to the rule Regulations Governing Establishment of Internal Control Systems by Public Companies issued by The Securities and Futures Bureau of Financial Supervisory Commission of Executive Yuan R.O.C., the Audit center formulates annual audit plans based on the results of the risk assessment. The annual audit plans include as audit items, at least, the control activities for major financial or business activities, such as for acquiring or disposing of assets, engaging in derivatives transactions, extending loans to others, granting endorsements or guarantees for others, supervision and management of subsidiaries, information flow security inspection, and major transaction cycles such as the sale and receipt cycle and purchase and payment cycle.

(3).Corrective action:

Internal auditors conduct the audit work of operation systems according to the annual audit plans to ensure that the established systems are efficient and are being met, information is reliable, operations are effective and timely. Internal auditors should report the result of their audit work and make recommendations.

(4).To report to the FSC via the Internet-based information system:

- To report to the FSC for recordation its next year's audit plan by the end of each fiscal year in the prescribed format.

- To report to the FSC for recordation and training of internal auditors by the end of January each fiscal year in the prescribed format.

- To report on the execution of its previous year's annual audit plan within two months from the end of each fiscal year in the prescribed format.

- To report the Internal Control System Statement within four months from the end of each fiscal year in the prescribed format.

- To report to the FSC for recordation its corrections of any defects and irregularities of the internal control system discovered during the past year's internal auditing within five months from the end of each fiscal year in the prescribed format.

(5). The appointment, dismissal, evaluation, salary and compensation of internal auditors :

According to the『Corporate Governance Best Practice Principles』Article 3 that the appointment, dismissal, evaluation, salary and compensation of internal auditors that shall be reported to the board of directors or shall be submitted by the chief auditor to the board chairperson for approval.

The『Corporate Governance Best Practice Principles』has been uncoverd in the corporate governance area of the company′s official website.

The『Corporate Governance Best Practice Principles』has been uncoverd in the corporate governance area of the company′s official website.

(6).The Internal Control System Statement:

- The self-inspection reports of departments and subsidiaries shall be reviewed by audit center. These reports, combined with the corrections of any deficiencies or irregularities of the internal control system discovered by the internal auditors, will be the main references for the Board of Directors and the General Manager in evaluating the overall effectiveness of the internal control system and issuing the Internal Control System Statement.

- The Internal Control System Statement over the years, please reference the following attached file.